》Check SMM spot aluminum quotes, data, and market analysis

》Subscribe to view historical price trends of SMM metal spot prices

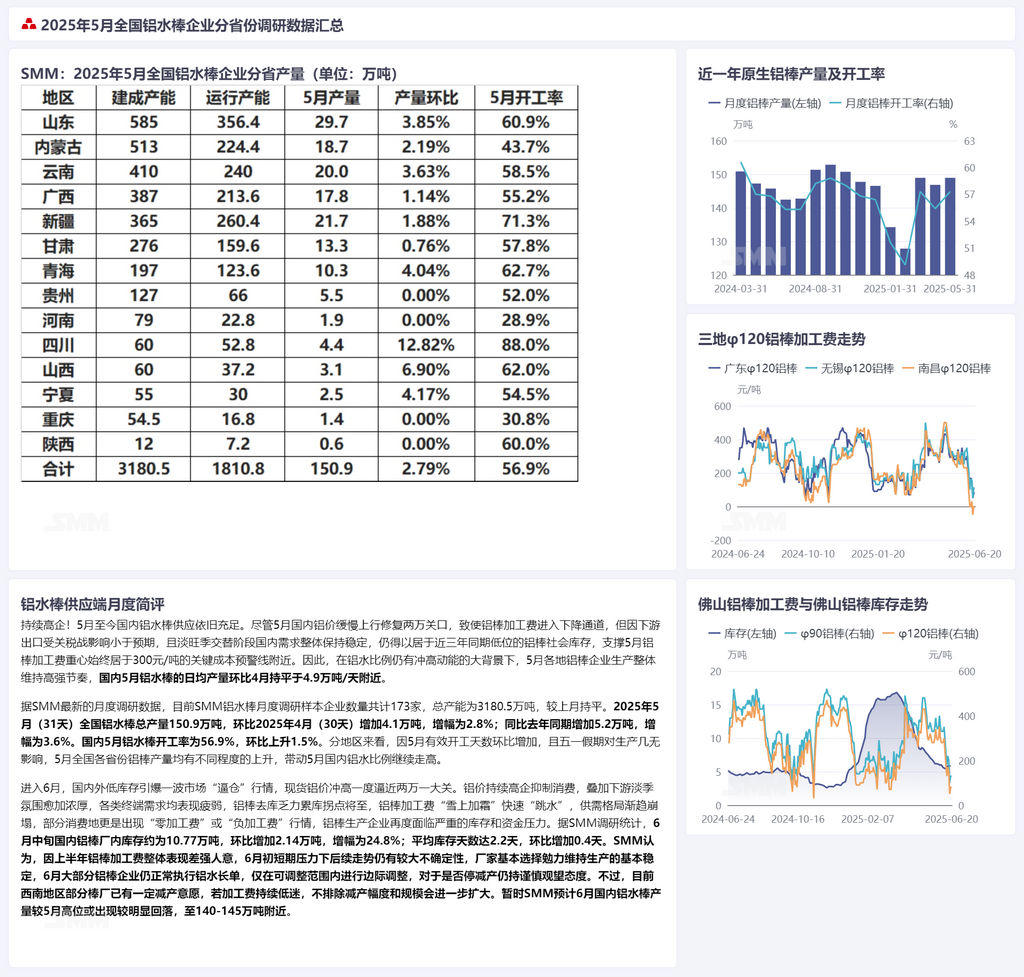

SMM News on June 22:

Remaining High! Domestic primary aluminum billet supply has remained abundant since May. Despite the slow upward movement of domestic aluminum prices in May, which repaired the 20,000 yuan/mt threshold, causing aluminum billet processing fees to enter a downward trajectory, the impact of tariff wars on downstream exports was less than expected. Additionally, during the transition between the off-season and peak season, domestic demand remained generally stable. As a result, social inventories of aluminum billets stayed near the low levels of the same period in the past three years, supporting the center of aluminum billet processing fees to remain near the key cost warning line of 300 yuan/mt. Therefore, against the backdrop of the liquid aluminum proportion still having upward momentum, aluminum billet enterprises across the country maintained a high-intensity production pace in May. The daily average production of domestic primary aluminum billets in May remained flat MoM at around 49,000 mt/day compared to April.

According to the latest monthly survey data from SMM, there are currently 173 enterprises in the SMM monthly survey sample for primary aluminum billets, with a total capacity of 31.805 million mt, unchanged from the previous month. In May 2025 (31 days), the total domestic production of primary aluminum billets was 1.509 million mt, an increase of 41,000 mt or 2.8% MoM from April 2025 (30 days), and an increase of 52,000 mt or 3.6% YoY from the same period last year. The operating rate of domestic primary aluminum billets in May was 56.9%, up 1.5% MoM. Regionally, due to the increase in effective operating days MoM in May and the minimal impact of the Labour Day holiday on production, aluminum billet production in various provinces across the country increased to varying degrees, driving the domestic liquid aluminum proportion to continue rising in May.

Entering June, low domestic and overseas inventories triggered a wave of market "cornering" sentiment, with spot aluminum prices surging and once approaching the 20,000 yuan/mt threshold. The sustained high aluminum prices suppressed consumption, coupled with the increasingly strong off-season atmosphere in the downstream sector, leading to weak performance in various types of end-use demand. The aluminum billet destocking momentum was sluggish, and the turning point for inventory buildup was approaching, causing aluminum billet processing fees to "plummet" further. The supply-demand pattern gradually collapsed, with some consumption areas even experiencing "zero processing fees" or "negative processing fees." Aluminum billet producers once again faced severe inventory and capital pressures. According to SMM survey statistics, in-plant inventories of domestic aluminum billet enterprises were approximately 107,700 mt in mid-June, an increase of 21,400 mt or 24.8% MoM, with an average inventory duration of 2.2 days, up 0.4 days MoM. SMM believes that due to the overall satisfactory performance of aluminum billet processing fees in H1, there is still significant uncertainty in the subsequent trend under the short-term pressure in early June. Producers are basically choosing to maintain a basic level of stable production. Most aluminum billet enterprises are still normally executing long-term contracts for liquid aluminum in June, making only marginal adjustments within adjustable ranges, and maintaining a cautious wait-and-see attitude towards production cuts. However, some billet producers in south-west China currently have a certain willingness to cut production. If processing fees continue to remain low, it cannot be ruled out that the extent and scale of production cuts will further expand. For the time being, SMM expects that the domestic production of primary aluminum billets in June may see a relatively significant pullback from the high level in May, reaching approximately 1.4-1.45 million mt.

Data source: SMM Click on the SMM industry database for more information